Hey there, business owner. If you’re reading this in 2026, chances are you’ve poured your heart, time, and savings into your company. Maybe it’s that cozy café you opened last year, the freelance design studio you run from home, or the growing construction crew that’s finally turning a profit. Whatever your story, one thing is certain: the wrong (or missing) business insurance can wipe it all out in a single lawsuit, storm, or cyber attack.

I’ve seen it happen too many times — a small business owner skips “that extra coverage” to save a few bucks, only to face a $150,000 claim that forces them to close doors. In 2026, with cyber threats exploding, extreme weather becoming the new normal, and customers quicker than ever to sue, choosing the right business insurance isn’t optional. It’s survival.

This complete 2026 guide will walk you through everything — step by step — so you can make smart, confident decisions. No jargon overload. No sales pitch. Just practical, up-to-date advice based on the latest industry data from MoneyGeek, Insureon, NerdWallet, and real small business experiences. By the end, you’ll know exactly what coverage you need, what it should cost, and how to buy it without overpaying.

Let’s get started.

Why Business Insurance Matters More Than Ever in 2026

The business world has changed fast. According to recent 2026 reports, the average cyber claim now tops $1 million for many small businesses. Natural disasters are hitting harder and more frequently. Lawsuits for slip-and-falls, data breaches, and even social media posts are on the rise. One bad day — a customer trip, an employee injury, or a hacked website — can bankrupt you if you’re not protected.

Here’s the reality check:

- Over 40% of small businesses that suffer a major loss never reopen.

- Workers’ compensation claims alone cost U.S. businesses billions every year.

- Cyber insurance uptake jumped again in 2025–2026 because ransomware attacks on small firms doubled.

Yet many owners still think, “It won’t happen to me.” Or worse, they buy the cheapest policy they find online without understanding what’s actually covered. That’s a recipe for disaster.

The good news? When you choose the right business insurance, you’re not just buying peace of mind — you’re protecting your livelihood, your employees, your family, and your future growth. And in 2026, the right policy can actually save you money through bundled discounts and proactive risk management credits.

The Most Common Types of Business Insurance You Need to Know

Before you can choose the right coverage, you have to understand what’s out there. Here’s a clear breakdown of the main types small businesses actually use in 2026:

| Type of Insurance | What It Covers | Who Needs It Most? | Average Monthly Cost (2026) |

| General Liability | Bodily injury, property damage, advertising injury, customer lawsuits | Almost every business | $45 – $100 |

| Business Owner’s Policy (BOP) | Bundles General Liability + Property + Business Interruption | Retail, restaurants, offices, small shops | $52 – $83 |

| Workers’ Compensation | Employee injuries, medical bills, lost wages (required in most states) | Any business with employees | $100 – $250+ (payroll-based) |

| Professional Liability (E&O) | Mistakes, negligence, faulty advice | Consultants, lawyers, accountants, IT pros | $37 – $150 |

| Commercial Property | Buildings, equipment, inventory, furniture against fire, theft, storms | Businesses with physical locations/assets | $100 – $200 |

| Commercial Auto | Vehicles used for business (deliveries, job sites) | Contractors, delivery services, sales teams | $150 – $300+ |

| Cyber Liability | Data breaches, ransomware, customer data loss, legal fees | Any business handling customer data | $50 – $150 |

| Business Interruption | Lost income if you have to shut down temporarily | All businesses (often included in BOP) | Bundled in BOP |

Pro tip: Most small businesses start with a BOP because it gives you the biggest bang for your buck. Then add workers’ comp (if you have employees) and cyber coverage (because 2026 threats are no joke).

Other specialized policies exist too — like product liability for manufacturers, liquor liability for bars, or tools & equipment insurance for contractors. Don’t guess. Match the coverage to your actual risks.

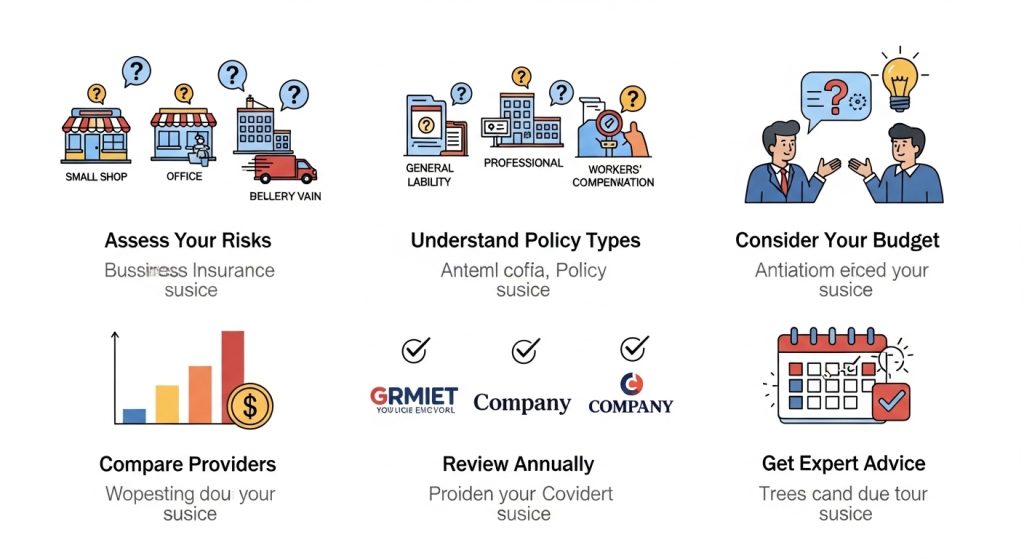

Step-by-Step: How to Choose the Right Business Insurance in 2026

Choosing the right policy doesn’t have to feel overwhelming. Follow these 7 practical steps:

- Assess Your Unique Risks Walk through your daily operations. What could go wrong? A customer slips in your store? An employee gets hurt on a job site? A hacker steals client emails? Write down your biggest worries. This is your risk profile — and the foundation of every smart insurance decision.

- Check Legal and Contractual Requirements Workers’ compensation is required in nearly every state once you hire your first employee (Texas is one notable exception). Landlords often demand general liability. Big clients may require proof of $1M+ coverage. Use your state’s labor department website or talk to a local agent.

- List Your Assets and Operations Do you own a building? Lease space? Have company vehicles? Store expensive equipment? Handle sensitive customer data? The more you have, the more coverage you’ll need.

- Decide on Coverage Limits and Deductibles Higher limits = higher premium, but better protection. A good rule of thumb: at least $1 million per occurrence for liability. Choose a deductible you can comfortably pay out of pocket.

- Bundle Where It Makes Sense A BOP can save you 20–30% compared to buying policies separately. Adding cyber or commercial auto to the same carrier often unlocks extra discounts.

- Get Multiple Quotes Never accept the first price. Shop at least 3–5 carriers. Use online quote tools from Insureon, The Hartford, or Progressive, but also talk to an independent agent for personalized advice.

- Review Annually Your business changes — revenue grows, you hire staff, you add new services. Review your policy every year (or after any big change) to avoid gaps.

Key Factors That Affect Your 2026 Insurance Costs

Insurance companies don’t pull numbers out of thin air. Here’s what actually moves your premium in 2026:

- Industry Risk Level — Contractors and restaurants pay more than consultants or online businesses.

- Location — High-crime or hurricane-prone areas cost more.

- Number of Employees — More staff = higher workers’ comp.

- Revenue & Claims History — Clean record? Lower rates.

- Coverage Limits & Deductibles — Higher protection = higher cost.

- Risk Management Practices — Security cameras, cybersecurity training, safety programs can earn you discounts.

Real 2026 Cost Snapshot (averages for small businesses):

| Industry | Typical Monthly Cost (Full Coverage) | Notes |

| Consultants / Freelancers | $80 – $225 | Low risk, mostly E&O + GL |

| Retail Stores | $150 – $350 | BOP + Property |

| Restaurants / Food Service | $250 – $600+ | High foot traffic + liquor liability |

| Contractors / Trades | $265 – $500+ | Workers’ comp is big here |

| Tech / IT Services | $100 – $300 | Cyber is essential |

| Healthcare Providers | $150 – $400 | Professional liability key |

(Data drawn from MoneyGeek, Insureon, and Simply Business 2026 reports.)

Top Business Insurance Providers in 2026 — Honest Comparison

After reviewing the latest ratings, here are the standouts:

| Provider | Best For | Average BOP Cost | Customer Satisfaction | Standout Feature |

| The Hartford | Overall / Most businesses | Very competitive | Excellent | Strong bundles + fast claims |

| Chubb | High-value assets & global reach | Higher | Top-tier | Premium coverage & service |

| Progressive | Commercial auto + small fleets | Affordable | Very good | Easy online tools |

| Travelers | Construction & service businesses | Competitive | Strong | Industry-specific expertise |

| Hiscox | Freelancers & startups | Lowest for solos | Excellent | Fast online quotes |

| Nationwide | Franchises & multi-location | Good | Reliable | Workers’ comp specialists |

My take: The Hartford consistently ranks #1 for most small businesses in 2026 because they balance price, coverage, and claims service. But if you’re a solo freelancer, Hiscox or NEXT Insurance might be cheaper and simpler.

How to Compare Quotes Like a Pro

Don’t just look at the bottom-line price. Compare these four things side-by-side:

- What’s actually covered (read the fine print!)

- Exclusions and limitations

- Claims process and customer reviews

- Discounts for bundling or safety measures

Pro move: Use an independent insurance broker. They work for you, not the insurance company, and can often find better deals.

Common Mistakes to Avoid in 2026

- Buying the cheapest policy without reading it.

- Assuming your homeowner’s or personal auto policy covers business use.

- Skipping cyber insurance because “we’re too small.”

- Forgetting to update coverage after hiring staff or expanding.

- Relying only on online quotes without speaking to a real agent.

Real Business Owner Stories (2026 Edition)

Take Sarah, who runs a small bakery in Texas. She thought her basic BOP was enough — until a customer had an allergic reaction and sued. Her policy covered the legal fees and settlement. Without it? Game over.

Or Mike, a freelance web designer. A client claimed his site caused them to lose $40k in sales. His professional liability policy handled the whole thing while he kept working.

These aren’t hypotheticals. They’re happening right now in 2026.

Frequently Asked Questions (FAQs)

Q1: Is business insurance required by law?

Not always, but workers’ compensation usually is if you have employees. Many contracts and landlords require general liability too.

Q2: How much does business insurance cost in 2026?

Most small businesses pay $500–$2,500 per year. It really depends on your industry and coverage needs.

Q3: Can I buy everything online?

Yes for simple policies, but complex needs (construction, restaurants) benefit from an agent.

Q4: Does cyber insurance cover ransomware?

Most policies do in 2026, including ransom payment (if chosen), lost income, and legal costs.

Q5: What if I work from home?

Your homeowner’s policy probably won’t cover business risks. You need at least a small business liability policy.

Q6: How often should I review my policy?

Every year, or whenever your business changes significantly.

Q7: Can I get a discount?

Yes — multi-policy, safety programs, claim-free history, and even installing security systems.

Final Thoughts: Protect What You’ve Built

Choosing the right business insurance in 2026 isn’t about checking a box. It’s about giving your company — and your family — the best possible chance to survive and thrive no matter what comes next.

Start today. Grab a notebook, list your risks, and get three quotes. Spend an afternoon now so you never have to spend a fortune (or lose sleep) later.

You’ve worked too hard to leave your business unprotected.

Ready to take the next step? Head to a trusted marketplace like Insureon or The Hartford’s small business portal and run some quick quotes. Or reach out to a local independent agent who understands your industry.

Your future self (and your business) will thank you.

Disclaimer

This article is for informational and educational purposes only. It is not intended as financial, legal, or insurance advice. Insurance policies and regulations vary by state and carrier. Always consult with a licensed insurance agent or broker and review your specific policy documents before making any decisions. Costs and coverage mentioned are general averages based on 2026 industry reports and can differ significantly based on your individual circumstances. SKHFA.com and the author are not liable for any losses or damages resulting from the use of this information.

Hasnain Raza is a dedicated insurance researcher and content writer with a strong passion for helping people make informed financial decisions. With deep knowledge of health insurance, auto insurance, and business insurance, he creates clear, accurate, and up-to-date guides for readers in Pakistan and the United States. Through SKHFA.com, Hasnain aims to simplify complex insurance topics so that individuals can protect their finances and choose the right coverage. This website is for educational and informational purposes only. Readers are advised to consult a licensed insurance professional before making any financial or insurance decisions.